|

|

|

Licenses

Contracts

Owners

Products

Market

3G Stocks

Layoffs

Live

Press Clips

EDGE

|

|

3G Market Shares: Infrastructure, User Equipment, Subscribers

|

|

Early September 2001 Nokia said it has 31 percent of the market for equipment based on WCDMA technology and it also claimed Ericsson has 30 per cent market share. Ericsson responded that it has 40 percent compared with Nokia's 30 per cent. Earlier Siemens claimed it would become the second largest 3G vendor and having also increased focus in Asia. Siemens' co-operation with NEC and R&D with China will help their effort. These three vendors are forming the top tier of WCDMA suppliers and are still fighting for market share.

Nortel got several key UMTS contracts earlier, but recently has been quiet. Motorola has been more successful in the cdma2000 market than in WCDMA sales. Lucent has sold WCDMA to Japan and almost to Germany, but it also needs more 3G big contracts. Alcatel also needs to increase its market share. Qualcomm and Samsung are only battling from cdma2000 market share, while Cisco tries to become a big 3G data equipment supplier.

UMTS Market Shares

Here is our ESTIMATION of UMTS (WCDMA) sales volume market share (mid 2003)

| Vendor

|

Our Estimation

|

Vendor's own estimation

|

| Ericsson

|

38 %

|

40 %

|

| Nokia

|

30 %

|

over 30 %

|

| Siemens (NEC)

|

18 %

|

20 %

|

| Nortel

|

11 %

|

15 %

|

| Alcatel (Fujitsu)

|

2 %

|

?

|

| Others *)

|

1 %

|

?

|

| Total

|

100 %

|

|

Market shares are only our estimations based on public information about UMTS contracts. Actual values may vary a lot. *) Others: Lucent, Motorola, Samsung, LG

3G Market Share Research

19. May 2004 Gartner via Unstrung and Siemens press release:

Last year Lucent ranked fourth in Gartners annual breakdown of worldwide mobile network infrastructure revenues for 2002, notching up an 11 percent market share behind runaway leader LM Ericsson at 29.5 percent; Nokia Corp. at 12.9 percent; and Siemens AG at 11.7 percent.

The analyst firms latest figures show a dramatic 3 percent fall in Lucent'c market share to 8 percent. Meanwhile Nokia and Siemens both increased their market standing on the back of a bevy of W-CDMA deals (14 and 13 percent respectively). Ericsson remains the market leader (26 percent).

According to the Gartner study, mobile operators invested 12 percent less than in 2002, or a total of US$ 40 billion. The seven top mobile infrastructure manufacturers had announced a total of 267 contracts. 64 percent of these contracts awarded last year were for GSM technology, 14 percent for CDMA networks and 14 percent for 3G/UMTS infrastructure.

With a market share of 23 percent, Siemens numbers among the worlds leading equipment suppliers. In Western Europe, Siemens received more 3G/UMTS contracts than any other supplier, and the first 3G/UMTS contract to come from Eastern Europe also went to Siemens.

4. March 2004 ABIResearch: "America's two premier infrastructure manufacturers are paying dearly for their lack of UMTS development. Lucent Technologies, a late arrival to the UMTS (Universal Mobile Telephone Service) marketplace, is managing to maintain an 11% share-of-market (SOM) in 2003, down from 17% in 2002. Motorola, on the other hand, has experienced a tumultuous drop in worldwide SOM, from 12% in 2002 to 4% in 2003.

While UMTS commands only an 18% unit share in 2004, it will skyrocket to almost 87% in 2009. ABI Research is forecasting a compound average annual growth (CAAG) rate of 52% for UMTS infrastructure from 2004 to 2009."

January 28, 2004 Mobility Infrastructure Market Grows 33% Q/Q in 4Q03,

According to DellOro Group. [More]

|

| Total WCDMA Infrastructure Revenues |

| Total Market |

4Q03 |

Qtr./Qtr. Growth |

| Manufacturer Revenues $B |

$1.1 |

+50% |

| Vendor |

Rank |

Growth |

| Ericsson |

1 |

+57% |

| NEC/Siemens |

2 |

+22% |

| Nokia |

3 | +90% |

| Fujitsu |

4 | +26% |

| Nortel |

5 | +169% |

|

|

January 28, 2004 According to a report published by DellOro Group, the total Mobility Infrastructure market (GSM/GPRS/EDGE, TDMA, CDMA, and WCDMA) will decline 1% in 2004 to $25.7 B, and then begin to rebound in 2005 with 5% growth. Growth is forecast to accelerate to 13% in 2006 on the strength of new deployments in China and CDMA 1X-EV-DO and DV upgrades. DellOro Group expects the total market, driven largely by WCDMA, to increase 7% in both 2007 and 2008, reaching $34.8 B in 2008. In 2006, WCDMA infrastructure revenues and base station shipments are set to surpass those of GSM-based systems. [More]

|

|

August 14, 2003 According to Dell'Oro Group, in 2Q03 mobility infrastructure revenues increased 1% to $6.5 Billion, compared to 1Q03. [More]

| Total Market |

2Q03

|

Qtr./Qtr.Growth

|

|

| Manufacturer Revenues $B |

$6.5

|

+1% |

|

| |

|

|

|

| Vendor |

Rank

|

Growth |

|

| Ericsson |

1.

|

+3% |

|

| Nokia |

2.

|

+23% |

|

| Nortel |

3.

|

+2% |

|

| Siemens |

4.

|

-4% |

|

|

|

May 15, 2003. According to Dell'Oro Group, in 1Q03 mobility infrastructure revenues declined 14% to $6.4 Billion, compared to 4Q02. [More]

| Total Market |

1Q03

|

Qtr./Qtr.Growth

|

|

| Manufacturer Revenues $B |

$6.4

|

-14% |

|

| |

|

|

|

| Technology |

Revenue

Growth

|

Base Station

Unit Growth |

Base Station

Price Change

|

| GSM/GPRS/EDGE |

-25%

|

-24% |

-4%

|

| CDMA |

-1%

|

+1% |

-1%

|

| TDMA |

+24%

|

+40% |

-7%

|

| WCDMA |

+25%

|

+33% |

-4%

|

|

|

February 14, 2003. According to Dell'Oro Group, in 2002 mobility infrastructure revenues declined 16% to $28.8 Billion. This figure included GSM/GPRS/EDGE, TDMA, CDMA (all variants) and WCDMA.

| Total Market |

2002

|

Year/Year Growth

|

| Manufacturer Revenues $B |

$28.8

|

-16%

|

| |

|

|

| Vendor |

Rank

|

Growth

|

| Ericsson |

1

|

-22%

|

| Nokia |

2

|

-14%

|

| Nortel |

3

|

-16%

|

| Lucent |

4

|

0%

|

| Siemens |

5

|

-8%

|

|

|

According to wireless data network market share article 09/12/02

from Wireless week.

Market Shares as of June 2002:

Ericsson 25%

Nortel 19%

Lucent 18%

Nokia 17%

Others 21% ?

|

|

|

Wireless Network Equipment Revenues per Quarter ($M) from Unstrung.com

|

1Q01 |

2Q01 |

3Q01 |

4Q01 |

1Q02 |

2Q02 |

3Q02 |

| Ericsson |

4,108 |

4,779 |

4,137 |

4,881 |

3,328 |

3,524 |

3,128 |

| Nokia |

2,046 |

1,919 |

1,879 |

1,980 |

1,453 |

1,492 |

1,564 |

| Siemens |

1,316 |

1,265 |

1,569 |

1,475 |

1,378 |

1,233 |

est. 1,200 |

| Nortel |

1,545 |

1,616 |

1,349 |

1,204 |

1,136 |

1,123 |

940 |

| Alcatel |

Not available |

NA |

NA |

759* |

759* |

759* |

759* |

|

|

|

|

|

|

|

|

Source: Company data, Wireless Oracle * = averaged from annual figure

The annual market is worth $34.3 billion

Motorola and Lucent Technologies reported third-quarter revenues of $1,014 million and $882 million, respectively. |

|

|

WCDMA Infrastructure Revenues:

| Total Market |

3Q02

|

Year/Year Growth

|

| Manufacturer Revenues $M |

791

|

+365%

|

| |

|

|

| Vendor |

Rank

|

Growth

|

| Ericsson |

1

|

n/a

|

| Nokia |

2

|

n/a

|

| NEC |

3

|

-11%

|

| Fujitsu |

4

|

-15%

|

- Published by Dell'Oro Group

|

|

Another view: 23rd January 2002 Opstock analyst Michael Schroder estimated "share of all reported 3G network orders" [W-CDMA only?] figures based on "108 deals to have been made by 62 different telecoms operators" looking at the number of deals:

Ericsson 31%

Nokia 28%

Copyright Reuters and 3G news+info+store. All rights reserved.

Another view: 5th February 2002

Reuters' article claimed "Ericsson ... is a supplier in 60 percent of all 3G network construction deals so far, which gives it a 40 percent global market share in terms of contract value."

Copyright Reuters. All rights reserved.

Yet another view: 3rd April 2002 Totaltele.com article wrote "[Siemens is] according to technology market research firm Yankee Group, is tussling with Motorola, Nortel and Lucent for third place in the market, where analysts see only three firms staying the course long term. Siemens has about seven percent of the market compared with 13 percent for Nokia and 30 percent for Ericsson, according to Yankee."

Copyright Totaltele.com. All rights reserved.

|

|

CDMA Equipment Market Shares by Revenue 4Q01-3Q02 (Source: Wireless Oracle):

Lucent 46%

Nortel 20%

Motorola 18%

Samsung 8%

Others 8%

Wireless Infrastructure Market Shares by Revenue 4Q01-3Q02; $48.1BN (Source: Unstrung):

Ericsson 32%

Nokia 13%

Siemens 11%

Lucent 11%

Motorola 10%

Nortel 9%

Alcatel 6%

Others 8%

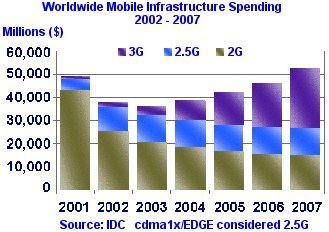

Relative Market Sizes

Worldwide Mobile Infrastructure Spending:

W-CDMA Network Equipment Forecast:

The full report is available at Unstrung Insider

3G will dominate the wireless infrastucture market in a near future:

Vendors will battle not only to push their products, but also their technologies! Here is our estimation how different geographical markets will be divided between technologies.

3G (cdma2000 and WCDMA) market sizes around 2005:

Asia / Pacific ~ 40% ; mixed and cdma2000, WCDMA and Chinese TD-SCDMA market. WCDMA will probably get larger market share that cdma2000. Japan and Korea will have cdma2000 and WCDMA networks. Taiwan will have one cdma2000 network and three or four WCDMA networks and Australia one or two cdma2000 and four WCDMA networks. Rest of the countries excluding China will pre-dominantly have WCDMA. GSM 1x might enter the market. Asia / Pacific ~ 40% ; mixed and cdma2000, WCDMA and Chinese TD-SCDMA market. WCDMA will probably get larger market share that cdma2000. Japan and Korea will have cdma2000 and WCDMA networks. Taiwan will have one cdma2000 network and three or four WCDMA networks and Australia one or two cdma2000 and four WCDMA networks. Rest of the countries excluding China will pre-dominantly have WCDMA. GSM 1x might enter the market.

Europe (East & West) ~ 30% ; WCDMA market. Europe (East & West) ~ 30% ; WCDMA market.

Americas (North & South) ~ 30% ; mixed and cdma2000, GPRS/EDGE and possibly future WCDMA market. Cdma2000 is struggling to get the market share at the moment. In the USA, government has long term plans to allocate new 3G spectrum so WCDMA has to wait. Cingular decided to change form cdma to GSM/GPRS/EDGE technology to provide 3G services. Verizon will have cdma2000 technology and AT&T Wireless and VoiceStream will implement GSM/GPRS/EDGE . South American cdmaOne networks will migrate to cdma2000 and GSM operators to WCDMA. Americas (North & South) ~ 30% ; mixed and cdma2000, GPRS/EDGE and possibly future WCDMA market. Cdma2000 is struggling to get the market share at the moment. In the USA, government has long term plans to allocate new 3G spectrum so WCDMA has to wait. Cingular decided to change form cdma to GSM/GPRS/EDGE technology to provide 3G services. Verizon will have cdma2000 technology and AT&T Wireless and VoiceStream will implement GSM/GPRS/EDGE . South American cdmaOne networks will migrate to cdma2000 and GSM operators to WCDMA.

Africa / Near East ~ several % ; mainly WCDMA market. Africa / Near East ~ several % ; mainly WCDMA market.

|

|